Is the Canmore Real Estate Market starting to recover?

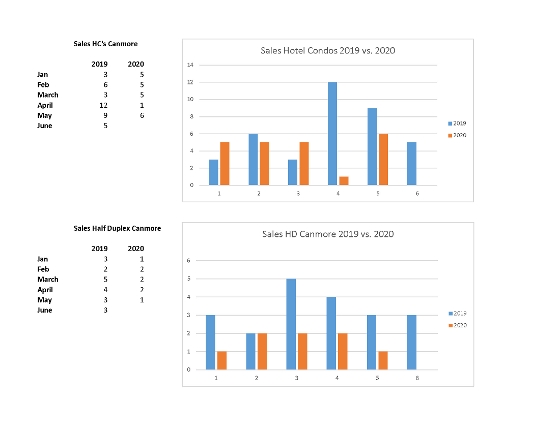

Comparing the sales data from 2019 with 2020 it sure looks like it! April 2020 shows a huge difference between 2019 and 2020 but May looks more promising. Interestingly prices have not come down except perhaps for a handful of hotel condo properties which sold quickly. Overall prices have remained rather stable. The amount of listings has not overly increased.

I will keep you posted as soon as the data for June is in!

I will keep you posted as soon as the data for June is in!